What It Means for Businesses and Regulators in Kenya

Global financial reporting continues to evolve as the IASB works to improve transparency and comparability in financial statements. One of the upcoming standards expected to shape reporting in regulated industries is IFRS 20 – Regulatory Assets and Regulatory Liabilities.

This forthcoming standard addresses a longstanding gap in financial reporting for entities operating under rate regulation, such as utilities and infrastructure providers. For countries like Kenya, where sectors such as energy, water, and transport operate under regulatory oversight, understanding IFRS 20 will be critical for accountants, auditors, regulators, and investors.

Understanding Rate-Regulated Activities

Many essential services are provided under regulatory frameworks that control the prices companies charge customers. Regulators set tariffs or price structures to ensure services remain affordable while allowing companies to recover their costs and earn a reasonable return.

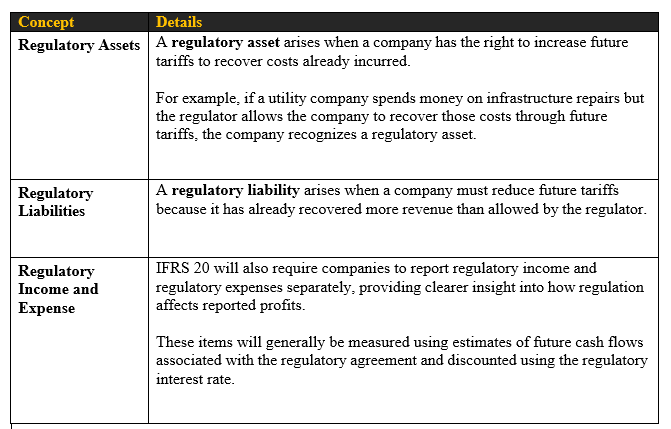

Under such arrangements, the timing of when a company incurs costs and when it recovers those costs through customer tariffs may differ. This timing difference gives rise to regulatory assets or regulatory liabilities.

The forthcoming IFRS 20 will provide a consistent accounting model to capture these effects in financial statements. It will require entities subject to rate regulation to recognize regulatory assets, regulatory liabilities, regulatory income, and regulatory expense so that investors can better understand how regulation affects financial performance and financial position

Why IFRS 20 Is Being Introduced

Historically, IFRS did not provide a comprehensive framework for accounting for the effects of rate regulation. Some entities used IFRS 14 Regulatory Deferral Accounts Accounts, but this was only intended as a temporary solution.

The IASB therefore developed IFRS 20 to establish a clear and consistent accounting framework for companies operating in regulated environments. The new standard is expected to replace IFRS 14 once issued.

The main objective of IFRS 20 is to ensure that financial statements reflect the economic reality of regulatory agreements, particularly where the compensation for goods or services supplied in one period is recovered through regulated prices in a different period.

Key Concepts Introduced by IFRS 20

Consider this:

A power distribution company incurs Ksh 500 million to repair critical electricity infrastructure after weather damage. However, the regulator allows the company to recover this cost through a tariff increase spread over the next five years.

Under IFRS 20:

- The unrecovered portion of the repair cost would be recognized as a regulatory asset.

- As customers pay higher tariffs in future years, the regulatory asset gradually reduces.

Without this accounting treatment, the company’s financial statements might show a large loss in the year of repair, even though the cost will ultimately be recovered from customers.

Relevance to the Kenyan Context

Kenya has several sectors where rate regulation plays a significant role, making IFRS 20 particularly relevant.

Energy Sector

Electricity tariffs are regulated by the Energy and Petroleum Regulatory Authority (EPRA). Power distributors or generation companies may incur costs that are later recovered through approved tariff adjustments.

Water Utilities

Water service providers regulated by the Water Services Regulatory Board (WASREB) operate under tariff structures that determine how operational and capital costs are recovered.

Transport and Infrastructure

Public transport concessions, toll roads, and airport services may also operate under regulatory frameworks where charges are controlled by government authorities.

In these sectors, IFRS 20 will help ensure that financial statements accurately reflect the economic impact of regulatory decisions.

Implications for Kenyan Businesses

Organizations operating in regulated sectors should begin preparing for the implications of IFRS 20.

Key areas of focus include:

1. Accounting systems and processes Companies may need to enhance systems to track regulatory assets and liabilities separately.

2. Financial statement presentation The standard will introduce new line items such as regulatory income and regulatory expense.

3. Regulatory agreement analysis Entities will need to carefully evaluate regulatory frameworks to determine whether they fall within the scope of IFRS 20.

4. Impact on financial performance indicators The recognition of regulatory assets and liabilities may affect profitability trends, leverage ratios, and valuation metrics.

Expected Timeline

The IASB is expected to issue IFRS 20 in 2026, with the standard anticipated to become effective for annual reporting periods beginning on or after 1 January 2029.

This timeline gives companies several years to prepare for implementation

Read also about Internal Audit vs External Audit.

How Aura & Co. CPA Can Help

Preparing for new IFRS standards requires technical expertise and early planning. We support organizations in navigating evolving financial reporting requirements through:

- IFRS implementation advisory

- Technical accounting guidance

- Financial reporting reviews

- Training for finance teams

- Regulatory impact assessments

For businesses operating in regulated sectors, understanding the implications of IFRS 20 early can help ensure a smoother transition once the standard becomes effective.

Contact us today on tax@aura-cpa.com, call us on 0769 111000 to learn more. You can also visit us at Haven Court, 1st Floor, Waiyaki Way, Westlands, Nairobi.